No Tax on Tips, Overtime & Car-Loan Interest—But Only If You Act Fast

If you’ve been scrolling through the news feeds since July 4th, you’ve likely heard whispers of “no tax on tips” or “overtime pay is tax-free now.” It sounds almost too good to be true—and in many ways, it is. The Tax Relief for American Families and Workers Act of 2025 (a.k.a. the “Big Beautiful Tax Bill”) temporarily excludes up to:

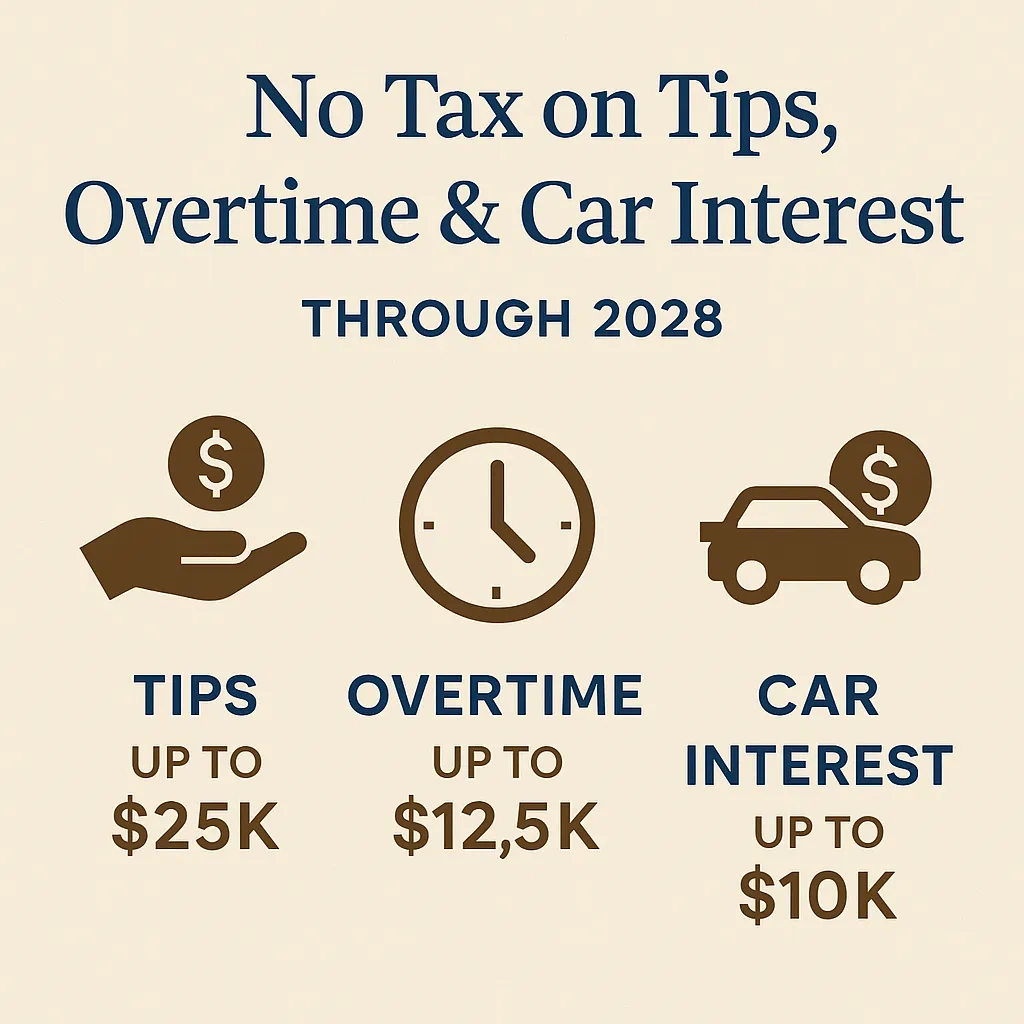

$25,000 of reported tip income

$12,500 of overtime pay

$10,000 of interest on a new-car loan

But these breaks only apply to tax years 2025–2028, and each has its own income caps and reporting requirements. Miss the window—or misunderstand the rules—and you’ll leave money on the table (or worse, trigger an IRS audit).

1. Tip Income Exclusion: Know the Limits

“No tax on tips is temporary… it’s income-based and capped. Maximum potential savings of $6,000—but likely closer to $3,000 for most.”

– Tonya in our July webinar

How it works: If a service occupation of yours is on the IRS’s official tip list, you can deduct up to $25,000 of tip income above the line—meaning before your adjusted gross income. Phase-outs begin at $150K (single) / $300K (MFJ) and end at $275K / $425K.

“Employers still report your tips on your W-2 or 1099. We just get to exclude them from federal income tax.”

– Tonya

2. Overtime Pay Exclusion: Hours Matter

Just like tips, legally paid overtime—over 40 hours weekly or 8 hours daily—can be excluded, up to $12,500 per individual (or $25K married filing jointly). Same 2025–2028 window and phase-out caps as tips.

Why it matters to you: If you bill extra project hours, run weekend workshops, or pick up consulting gigs, this exclusion can save hundreds or even thousands in federal tax each year.

3. New-Car Interest Deduction: Act Now

Buying a new vehicle? Interest on your first-lien, U.S.-assembled auto loan for vehicles under 14,000 lbs qualifies for up to $10,000 of above-the-line deduction. Phase-outs begin at $100K / $200K AGI.

Pro tip: You must report the VIN on your return, and lenders will issue a new-style 1098-INT for auto interest.

What’s the Catch?

Temporary and Income-Limited: All three breaks expire after 2028 and disappear entirely if your AGI exceeds the specified thresholds.

Documentation Is Key: Keep clear records—W-2s, 1099s, loan statements, and time logs—to prove eligibility.

“This is above-the-line, just like student-loan interest, so it helps whether you itemize or not.”

– Tonya

Don’t Wait—Lock In Your Savings

Implementing these exclusions correctly can be a tax minefield.

“We dug into the 940-page bill to make sure everything we’re telling you is truth from the bill,” Misty confessed in our webinar, so you don’t have to.

Ready to capture every dollar you deserve?

Watch our deep-dive webinar for all the details and live Q&A: Watch on YouTube »

Or book a Financial 360 now—we’ll map out which of these new exclusions apply to you and how they fit into a broader, multi-year savings plan.

We help with the stuff behind the scenes so you can make informed financial decisions, look at the big picture, and focus more on the fun parts of running your business.

Visit our website to book that call, and check us out on our other platforms:

@newsomecpa on Threads

@MistyNewsomeCPA on YouTube

Misty Newsome CPA LLC on Facebook

@newsomecpa on Instagram

Misty Newsome on LinkedIn